Why Long-Term Care Insurance Is Your Permission Slip to Spend

Bill Perkins' radical philosophy is simple: maximize life experiences and draw down your net worth to cross the finish line with exactly zero dollars left. But one terrifying question blocks the path for most people — What if I get sick? The fear of late-life medical emergencies causes us to oversave, sacrificing years of experiences to build a massive "just-in-case" safety net that often goes entirely untouched. Perkins' solution is clear: Long-Term Care (LTC) Insurance.

"Remember that you can buy long-term care insurance, which costs far less than self-insuring by saving massive amounts of money for a crisis that may never come." — Bill Perkins, Die with Zero

1. Eliminate the "Self-Insuring" Trap

Many people stash away $300,000+ specifically for potential healthcare crises in their 80s. If you die peacefully, you effectively worked for free during your prime years. An LTC policy shifts that massive, ambiguous liability to an insurance company — replacing uncertainty with a predictable, fixed premium.

2. Your Permission Slip to Spend

LTC insurance is an offensive tool, not just a defensive one. Once your assisted-living and healthcare costs are contractually covered, you receive a psychological green light. No more hoarding cash out of fear — you're free to spend on meaningful experiences, family gifts, and fulfillment while you still have the health and vitality to enjoy them.

3. A Realistic Check on End-ofLife Costs

Perkins shares a sobering story: his father's final days cost $50,000 per night in intensive care. His point is practical — saving an extra $50,000–$100,000 in your 40s won't cover a true catastrophic crisis. Fully self-insuring against the worst case is mathematically impossible. Insure what you can, protect your baseline, and maximize the life you have now.

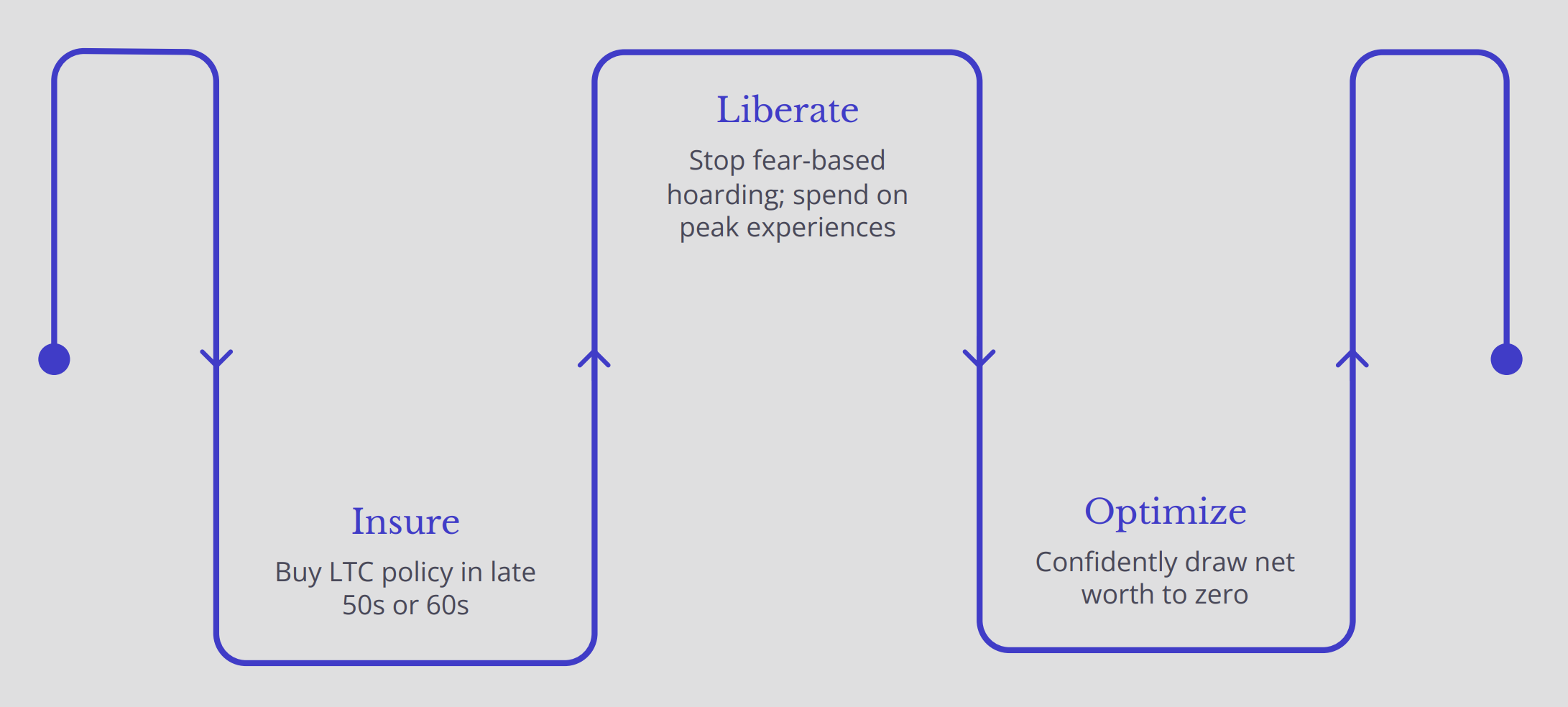

The Die with Zero Life Curve — Protected

Executing a perfect life curve requires essential guardrails. LTC Insurance protects your downside so a late-life health crisis can't drain your hard-earned wealth. With that safety net in place, you can confidently drive your net worth toward zero — converting every ounce of life energy into a life well-lived.

> Purchase LTC or hybrid life/LTC policy in your late 50s or early 60s — health ratings are better and premiums are lower before age 65

> Treat the premium not as an expense, but as the price of your financial freedom

> Redirect the capital you were hoarding for self-insurance into peak experiences now

💡 Action Step

Don't let the fear of a hypothetical future health crisis paralyze your present. Look into a long-term care insurance policy or hybrid life/LTC options in your late 50s or early 60s. The math is clear: a fraction of your capital spent on an LTC premium unlocks the freedom to spend the rest on what truly matters — a life fully lived.

- Self-insuring requires $300K+ set aside. An LTC policy costs a fraction of that — and covers far more.

The Die with Zero framework only works when the fear of catastrophic illness is neutralized. LTC Insurance is the missing piece that transforms a terrifying philosophical ideal into a practical, executable plan — giving you the confidence to spend boldly, live fully, and finish at zero.